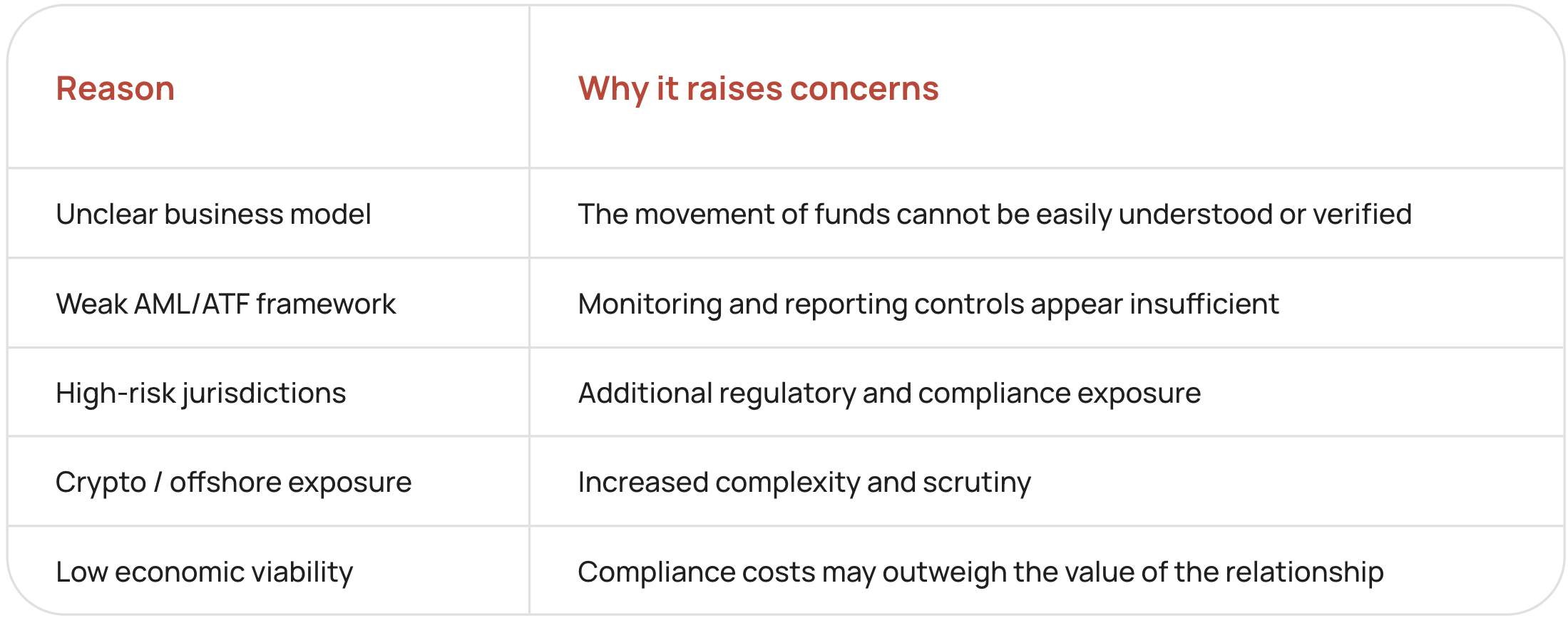

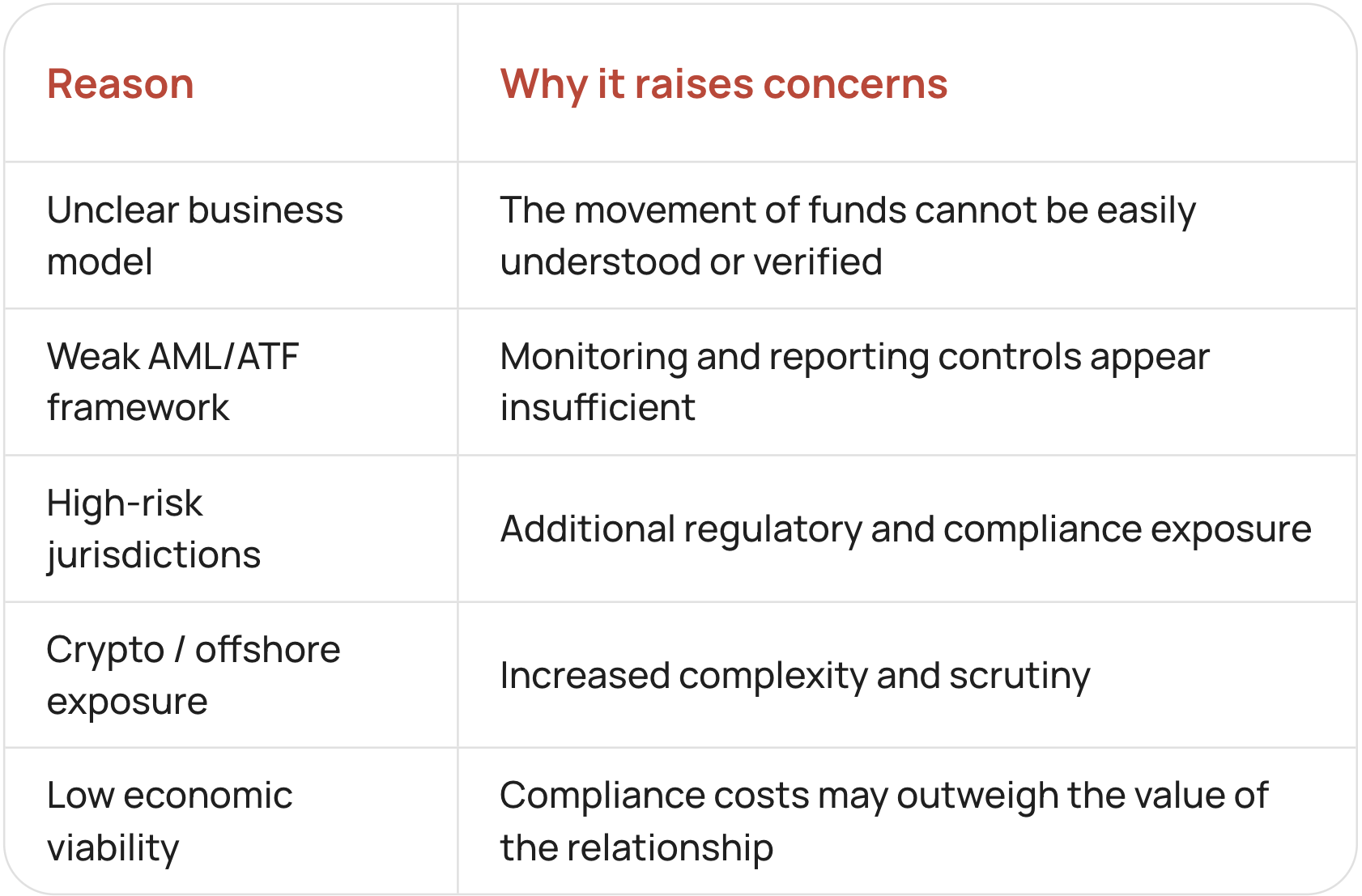

In most cases, the review starts with a simple reconstruction of the business: who uses the service, where the money comes from, how it moves through the system, and how each stage is controlled. When these elements are unclear or inconsistent, the level of uncertainty increases and the review becomes more restrictive, leading banks to focus on several key assessment areas.

The specific MSB model also shapes the banking assessment. A foreign exchange business serving local clients, a remittance provider, a virtual currency platform, and a B2B payment processor may all operate within the MSB sector, while presenting different transaction flows, counterparties, geographic exposures, and compliance requirements. Banks therefore assess the actual functions performed by the business, including whether it receives, holds, converts, or distributes client funds.

Business model

Banks want to understand how the company generates revenue and how money moves through the business. For example, a company that facilitates international money transfers will generally face more scrutiny than a business operating within a single market because the transaction flows are more complex.

Clients

The expected customer base is another important factor. Banks assess who will use the service, whether customers are individuals or businesses, and whether certain client groups may require enhanced due diligence.

Geography

The countries involved in transactions can significantly affect a bank's risk assessment. Cross-border activity is common for many MSBs, but some jurisdictions may require additional review because of sanctions, regulatory concerns, or higher financial crime risks.

AML/ATF framework

Banks look closely at how the company identifies customers, monitors transactions, and manages suspicious activity. A documented AML/ATF program carries more weight when it is clearly connected to the actual operations of the business.

Documentation

The ability to explain and support the business model with clear documentation often influences the overall review. This can include transaction flow descriptions, compliance policies, customer onboarding procedures, and operational forecasts.

.svg)